Ashley Furniture Financing Options: A Ruidoso Guide

You finally find the mattress that feels right. Maybe it's a pressure-relieving Tempur-Pedic, a supportive Sealy hybrid, or a plush Stearns & Foster that makes your shoulders drop the second you lie down. Then you look at the total and your brain shifts from “This is the one” to “How am I supposed to pay for this without stressing every month?”

That moment is common in Ruidoso, Alto, and across Lincoln County. A good bed is part comfort, part health decision, and part budget decision. If you're weighing ashley furniture financing options, the goal isn't just getting approved. It's understanding what kind of agreement you're signing so your better sleep doesn't come with a financial headache.

A quality mattress can support your body for years, which is why many families treat it as a long-term home investment. If you're thinking through that bigger picture, this guide on why a high-quality mattress matters for long-term health gives helpful context before you decide how to pay for one.

Table of Contents

- That Perfect Mattress and Its Surprising Price Tag

- Understanding the Ashley Advantage Credit Card

- Exploring Ashley's Lease-to-Own Path with Acima

- The Hidden Costs of Big-Box Financing

- A Smarter Local Alternative for Ruidoso Residents

- Financing Side-by-Side Ashley vs Miller Waldrop

- Your Local Financing Questions Answered

That Perfect Mattress and Its Surprising Price Tag

A couple comes into a showroom after sleeping badly for months. One partner wakes up with hip pressure. The other sleeps hot and tosses around all night. They try a few beds, land on a premium hybrid, and you can see the relief on their faces.

Then comes the second part of the conversation. Not comfort. Cost.

That's where many shoppers freeze. They aren't saying the mattress isn't worth it. They're trying to figure out whether the monthly payment will feel manageable once real life kicks back in. Groceries, kids' activities, cabin upkeep, heating bills in the mountain cold. It all counts.

Why the price feels bigger with sleep products

A mattress isn't like a lamp or accent chair. You use it every night, and if it's wrong, your back, neck, and shoulders remind you fast. Memory foam models can help with pressure point relief by distributing body weight more evenly. Hybrids can add bounce, airflow, and stronger edge support, which many active sleepers like.

That means the purchase often lands in an awkward middle ground. It's too important to buy carelessly, but expensive enough that many families want financing.

A smart financing choice should lower stress, not move it from your body to your budget.

What people usually want to know first

Most shoppers in Ruidoso ask versions of the same questions:

- How much do I need upfront?

- Will this require strong credit?

- Is this a store card, a loan, or a lease?

- What happens if I can't pay it off as fast as I hoped?

Those are the right questions. The hard part is that big retailers often package financing in language that sounds simple at first glance, but the details matter more than the headline.

Understanding the Ashley Advantage Credit Card

Ashley's main financing path is the Ashley Advantage™ Credit Card, which is handled through Synchrony. If you've seen an Ashley promotion for special financing, this is usually what they mean.

How the card works

At the basic level, it works like a retail credit card. You apply, the lender reviews your information, and if you're approved, you receive a credit line that can be used on qualifying Ashley purchases.

Ashley states that its long-running financing relationship with Synchrony began in 2010 and was renewed in 2025 after nearly 15 years. That program includes promotional offers such as no interest if paid in full within 6 months with no minimum online purchase, 12 months on $499+ online purchases, and 24 months special financing on $999+ purchases made with the Ashley Advantage Synchrony credit card, according to Ashley's financing page.

That's the part most shoppers notice first. The monthly path can look much more approachable than paying the whole amount at once.

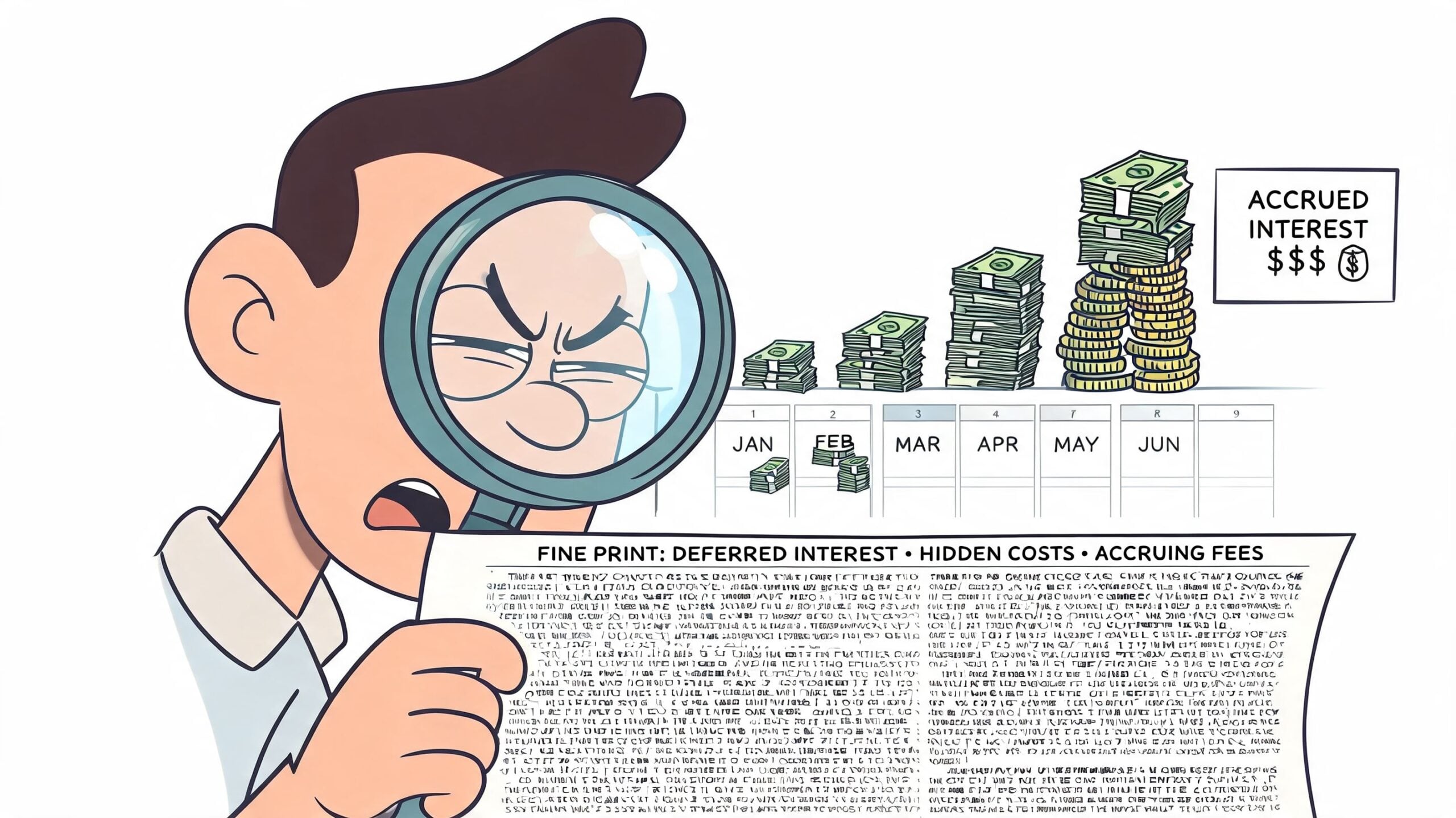

Where shoppers get tripped up

The phrase that deserves your full attention is “if paid in full.” That condition does a lot of work.

When a retailer advertises a promotional period, shoppers sometimes hear “interest-free” and stop reading. But store-card promotions often come with rules, deadlines, and minimum payment requirements. If you don't understand those terms before signing, the purchase can feel very different a few months later.

Consider the practical breakdown of your choices:

- You're opening a store-linked credit account.

- The purchase may qualify for a promotional window.

- You need to know exactly what ends that promotion, and when.

- You need a payoff plan before you swipe the card.

Practical rule: Don't ask only, “What's the monthly payment?” Ask, “What balance must be gone by what date?”

For some households, this kind of financing works well. If your budget is steady and you're organized about payment timing, a promotional plan can be useful. If your income changes month to month, or you're juggling multiple bills, the margin for error gets smaller.

Shoppers who want to compare local financing paths before deciding can review mattress financing options from a local Ruidoso sleep store.

Exploring Ashley's Lease-to-Own Path with Acima

Not everyone wants, or qualifies for, a retail credit card. That's where Ashley's Acima option enters the picture.

Lease-to-own is not the same as a credit card

Acima is a lease-to-own program. That means you're not using a traditional revolving credit card in the usual sense. You're leasing the item and gain ownership under the program's terms.

That distinction matters because shoppers often lump all financing into one mental bucket. It isn't one bucket. A store card, an installment plan, and a lease-to-own agreement can feel similar at checkout while working very differently over time.

Ashley's Acima page says the program offers no credit needed, includes a 90-day early purchase option, and can approve lease amounts up to $4,000. Ashley also notes that using the early purchase option can save 30% to 50% on total lease costs compared with carrying the full 12-month lease term. That information appears on Ashley's Acima financing page.

Why the 90-day option matters

This is the key detail in the whole Acima conversation. If you use lease-to-own, the cost can look very different depending on whether you exit early or stay in the agreement longer.

For a shopper focused on brands like Sealy or Stearns & Foster, that approval range may line up with many mattress purchases. But the smarter strategy is often not just “Can I get approved?” It's “Can I realistically use the early purchase option?”

Here's when Acima may appeal to a shopper:

- Credit challenges: You may not want a traditional card application.

- Urgent need: Your mattress has failed now, not six months from now.

- Thin credit file: You have income, but not much borrowing history.

And here's the caution:

- The short window matters: If you plan to use the early purchase benefit, you need a real plan for those first 90 days.

- Lease language matters: You should know when ownership transfers and what the full cost looks like if you don't purchase early.

If you're considering this route, treat the 90-day option like a deadline on your calendar, not a detail in fine print.

If you're exploring options designed for shoppers with tougher credit situations, this guide to mattress financing with no credit check considerations can help you compare the tradeoffs.

The Hidden Costs of Big-Box Financing

Big-box financing isn't automatically bad. The problem is that many shoppers hear the headline and miss the structure behind it.

Promotions can sound simpler than they are

A sign in a showroom or a banner online might say “special financing” or “no interest if paid in full.” That sounds friendly. It sounds easy. But these offers often reward precision, not guesswork.

If you don't know the due dates, payoff expectations, and what happens after the promotional period, you're making a budget decision with missing information. That's where people get frustrated. Not because financing exists, but because the language around it can feel cleaner than the actual agreement.

A few warning signs to watch for:

- Promotional wording without a payoff plan: If you haven't mapped how you'll clear the balance, you're still guessing.

- Focus on approval over affordability: Getting approved doesn't prove the terms fit your monthly life.

- Tiny details at the bottom: Those details usually control the outcome more than the big headline does.

Big-box financing often feels distant

There's another cost that doesn't show up on a statement. It's the cost of confusion when you need help.

With a national chain and a national finance partner, support can feel remote. You may be talking to a department, not a person who knows your purchase, your household, or your local situation in Lincoln County. If a term doesn't make sense, or a billing issue pops up, you're often working through a large system built for scale, not neighborly clarity.

Financing should feel understandable on the day you sign, not only after your first statement arrives.

That matters with sleep products because the decision already carries emotion. You're trying to solve back pain, overheating, partner motion transfer, or a worn-out guest room in a cabin. Adding confusion on the money side can make the whole purchase feel heavier than it needs to.

A Smarter Local Alternative for Ruidoso Residents

For many households, the better financing experience isn't about chasing the flashiest promotion. It's about clarity, conversation, and accountability close to home.

Local guidance changes the experience

When you work with a local sleep retailer, the biggest difference is usually simple. You can ask questions face to face.

That matters more than people think. Financing terms are easier to understand when someone slows down, explains the language plainly, and helps you match a payment path to your actual life. Not a generic average customer. Your life. Your budget. Your priorities.

In a family business environment, the conversation often centers on practical fit:

- Do you need pressure relief or firmer spinal support?

- Are you shopping for your home, a guest room, or a rental cabin?

- Do you need the lowest monthly obligation, or the clearest payoff structure?

That's a very different feeling from clicking through an impersonal application flow.

Sleep needs are personal in mountain communities

People around Ruidoso and Alto don't all shop the same way. Some families need a guest mattress that can handle frequent visitors. Some want a Tempur-Pedic for pressure relief after long days on their feet. Others need cooling features because dry mountain air and layered bedding can still leave them sleeping warm.

A local retailer can connect those comfort needs with financing in one conversation. That lowers the odds of buying the wrong bed for the wrong reason.

There's also peace of mind in having policies that help you feel protected after the sale. For shoppers who want budget confidence as part of the process, a local Low Price Promise can be part of that reassurance.

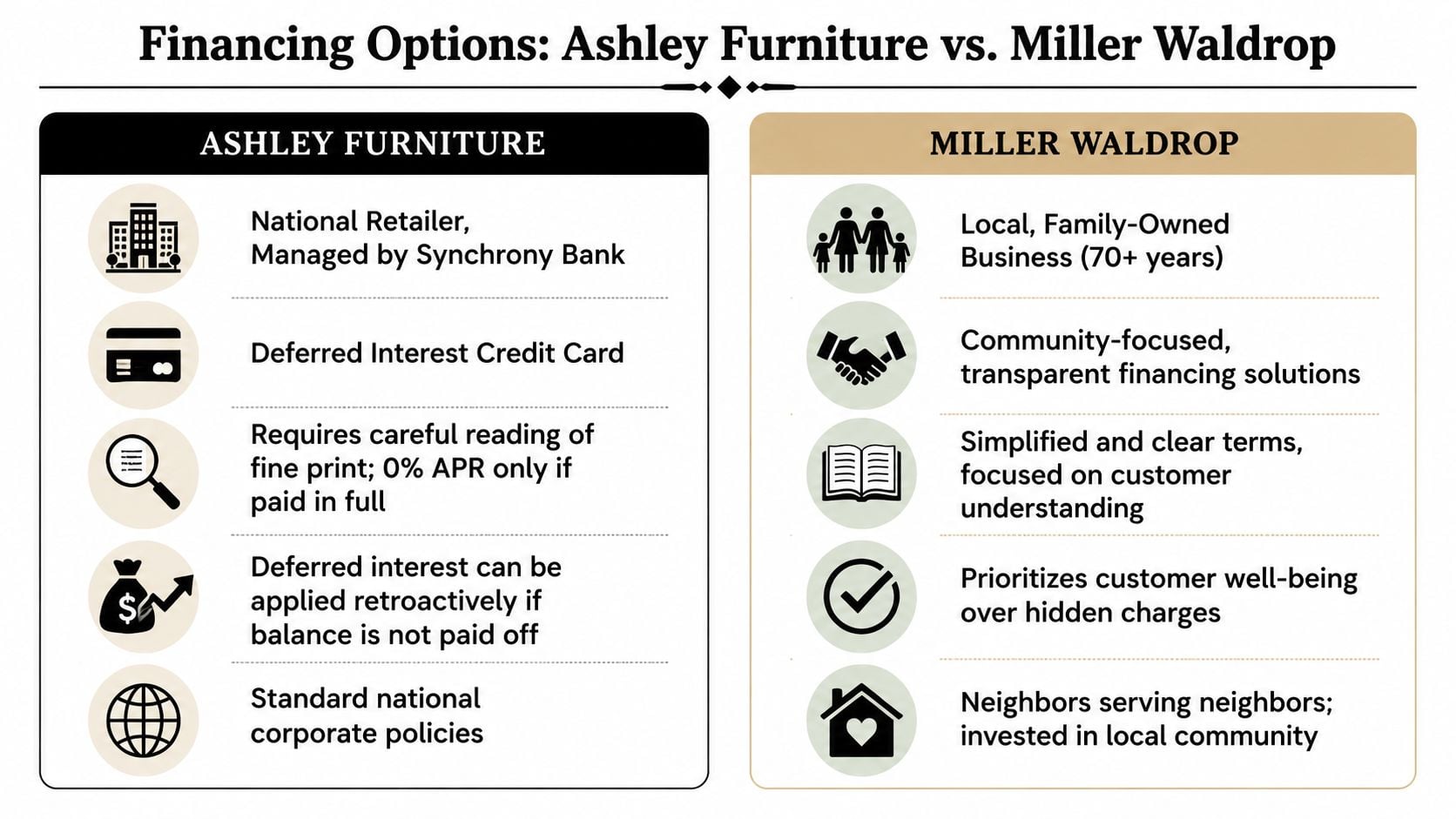

Financing Side-by-Side Ashley vs Miller Waldrop

When you compare financing choices clearly, the decision gets easier. You stop asking, “Which ad sounds best?” and start asking, “Which experience helps me sleep better, both physically and financially?”

What matters most when you compare

Ashley's financing paths can serve a purpose, especially for shoppers who want either a store card or a lease-to-own route. But the structure asks you to pay close attention to the terms. The burden is often on you to decode what kind of agreement you're entering and how timing affects the final cost.

A local, family-owned alternative usually feels different in three ways.

First, the conversation is more personal. Second, the explanations are often more direct. Third, your purchase isn't separated from your support. The same local business helping you choose between memory foam, hybrid, Sealy, Sherwood, or Stearns & Foster can also help you understand the payment path.

Good financing support isn't just about saying yes. It's about helping you avoid a yes that creates regret later.

For shoppers comparing post-purchase peace of mind too, it helps to review how mattress protection policies differ. This overview of the Ashley furniture mattress warranty question is useful alongside any financing decision.

Financing Comparison National Chain vs Local Expert

| Feature | Ashley Furniture (via Synchrony/Acima) | Mattress Pro by Miller Waldrop |

|---|---|---|

| Primary model | Mix of retail credit card and lease-to-own options | Local financing guidance centered on mattress purchases |

| Main experience | National retail system with third-party financing partners | Face-to-face help from a local sleep team |

| Best for | Shoppers comfortable reading and managing promotion details | Shoppers who want plain-language help and local accountability |

| Potential confusion point | Different financing structures can sound similar at checkout | Questions are typically handled in-store with direct explanation |

| Support style | Large-scale, corporate process | Relationship-based, community-focused service |

| Comfort protection mindset | Financing is separate from the mattress fitting experience | Financing can be discussed alongside comfort fit and purchase protections |

The biggest difference isn't just the paperwork. It's the feeling after the sale. In a local store, you're more likely to know where to go if you have a question, need delivery support, or worry you chose the wrong comfort level.

That's especially valuable with something as personal as sleep.

Your Local Financing Questions Answered

Can I finance a mattress if my credit isn't perfect

Yes, sometimes you can. The exact path depends on the retailer and the financing partner. Some programs are traditional credit-based offers, while others are lease-to-own arrangements that may be more accessible for shoppers with limited or challenged credit histories.

What does no interest if paid in full really mean

It means the promotional benefit usually depends on paying the qualifying balance within the stated period. If you're considering an offer like that, ask for the exact deadline, the required payment schedule, and what happens if the balance remains after the promotion ends.

Is lease-to-own a good idea

It can be useful when you need a mattress now and don't have a strong credit option available. But you need to understand that lease-to-own is not the same as a standard credit card. The early purchase terms, ownership timeline, and total cost matter.

Should I finance a mattress or wait

If your mattress is wrecking your sleep, waiting can carry its own cost in soreness, poor rest, and daily fatigue. Financing makes the most sense when the payment fits your budget and the terms are clear enough that you won't feel trapped later.

A few final questions to ask before signing anything:

- What kind of agreement is this? Credit card, installment financing, or lease-to-own.

- What's the payoff trigger? Know the exact date and condition.

- What happens if life gets busy? Ask about late payments, missed deadlines, and changes after the promotional period.

- Who helps me if I'm confused? A local answer is often easier than a hotline.

If you walk into any store on Sudderth Drive or elsewhere in Lincoln County with those questions ready, you'll make a better decision.

Ready to transform your sleep? Visit our Sleep Pros at Mattress Pro by Miller Waldrop located at 2801 Sudderth Drive, Suite F, in Ruidoso. From luxury brands to budget-friendly solutions, we're here to help you wake up loving your mornings. Browse our collection online or stop by Monday through Saturday.